By Sarah Foley

Debt in America has reached an all time high of $1.5 trillion, forcing people to put their lives on hold. Of course, the more known debt is credit card debt but what is the real underlying reason for this crippling debt in our economy? Student loans.

There are more than 44 million Americans with student loan debt, owing a total amount of about $1.5 trillion. Americans owe almost $600 billion dollars more in student debt than in credit card debt.

Quinnipiac University marketing professor Maxim Polonsky says that this debt is due to students being uninformed about student debt while picking the school that they want.

“It is unfortunate that student are in this situation. A lot of students don’t know what they are signing up for,” Polonsky said. “So, there can be a lot more blame put on the consumer for not knowing what they are signing up for. Students are financially illiterate and they think it can just be dealt with tomorrow.”

There are many different types of loans that students can apply for if they are looking at a school that is out of their financial reach. Yet, of course these loans come with interest rates which can seriously change the amount expected to pay after graduation.

Last July, the Federal Board of Education decided to increase the interest rate on federal student loans from 4.45 to 5.05 percent this year.

To put this in perspective, say a student owes an average student debt of $30,000 after graduation. This debt will become an extra $3,195 instead of $2,800. To calculate your loans, click here.

Interest rates are rising because the Federal Reserve has been increasing interest rates on the Federal Funds rate. This influences the interest rates on other major loan indexes, especially Treasury rates and the LIBOR index. The interest rates on most private student loans are based on the 1-month and 3-month LIBOR indexes.

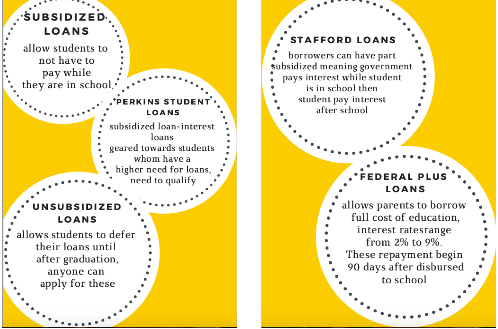

Federal student loans come in many forms to fit different needs.

These loans consist of:

Financial guru Mark Kantrotwitz, a writer for Private Student Loans, said, “Since we are in a rising interest rate environment, you can expect the interest rates on student loans to continue increasing by about 0.5 to 0.75 percent per year.”

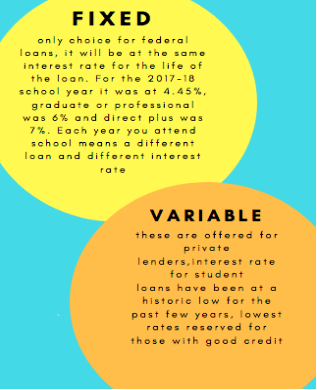

Federal education loans increase their interest rates once a year — on July 1 — based on the last 10-year Treasury Note auction in May. Private student loans, on the other hand, can change their interest rates as frequently as monthly.

Private Student Loans.guru provides unbiased and objective information about private student loans. Private student loans are offered by private lenders such as Citizens Bank, College Ave, LendKey, Sallie Mae. Private student loans can be fixed or variable.

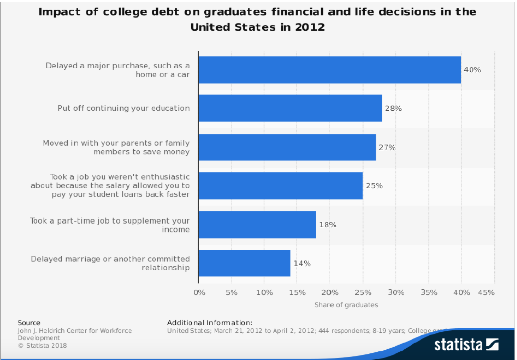

Students are well educated about needing to take loans out for college but the concept of interest rates usually flies under the radar. Students are delaying life decisions such as purchasing a house or car, furthering their education and getting married.

Although this is a huge struggle for most graduates there are ways to reduce this financial burden. Sofi is an online loan company that offers student loan refinancing options to students suffering from debt.

“We found over 60 percent of respondents reported that student loan debt is one of the top two financial concerns in their lives. While student loans are clearly a stressor for millennials, there’s a way to prevent them from causing students so much anxiety,” said a Sofi representative.

The loaning company holds events such as cocktail parties, cooking classes and yoga classes to help their clients feel more comfortable speaking out and connecting with others suffering from student loan debt. Sofi is the leading student loan provider refinancing over 250,000 people and has spent $18 billion in refinanced student loans.

Graduates can also qualify for student loan deductions through taxes but these deductions come with limitations. Loans can only be deducted if they were loaned from a qualified source, such as federal loans and private loan lenders. It is possible to deduct interest on student loans even if you don’t itemize your deductions.

This is helpful especially since grads are unlikely to own a house right away.

Offered to all is Public Student Loan Forgiveness. The program offers full student loan forgiveness to anyone who works in the public sector, which includes non-profit employees, Peace Corps volunteers, public school teachers and staff. The Pay as you Earn forgiveness program allows those struggling with student debt to make 240 payments of $65.92 a month. Once those 240 payments are complete, the rest of the debt will be forgiven.

Golden Financial services, a debt settlement company warns that, “thousands of qualified consumers won’t be getting student loan forgiveness on the public service program even though they believe they will because they forget to submit the form for it.”

The company blames this on the Department of Education and loan services for not clearly disclosing this to students. The application for student loan debt consolidation is here.

Working with a student loan attorney can be a serious next step when suffering with student debt. An attorney can help a grad navigate the complicated world of student debt and shed light on the concept of fixing it. They can help grads get out of default and on to a better repayment plan.

Student debt attorney Kevin McCarthy says he has seen an exponential growth of graduates coming for help.

“Most people come to us when they are living off of peanut butter and jelly sandwiches, not being able to help themselves whatsoever. Credit card debt allows people to to go bankrupt while student loan debt has to be paid off. This is causing a lot of pain for families and isn’t allowing people to live a better life,” he said.

An attorney can provide guidance regarding your legal rights and options, represent your interests by negotiating with your student loan holder, help you resolve defaults and apply for a discharge, and handle credit disputes. Attorneys can only help if the loans are from a private student loan lender. They cannot help if the student loans are federal.

Being well educated about loans and their interest rates can allow avoidance of crippling debt. Families struggling to understand student loans can hire a college funding adviser to help them work through the finances.

Central Mass college funding advisor Dave Landry said, “Many families feel overwhelmed with the college financial aid system. In my view, the system can also be unfair – especially if you make mistakes while navigating through the process.”

These advisers will stay with you throughout your time at school and help assist applying for loans to find ones that fit you best.

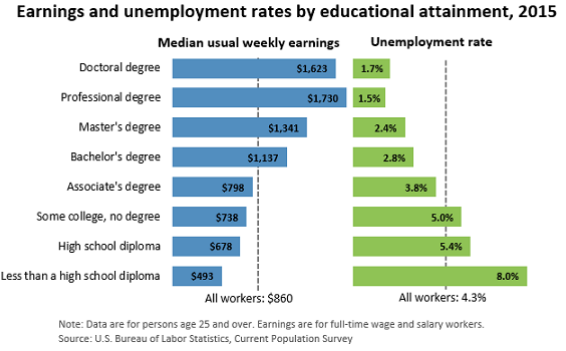

Although student loan debt sounds intimidating to most, it is also considered “good debt” because of its importance. Without an education, people struggle to increase their income opportunities. A recent study from Georgetown University found that those with a college education earn over $1 million in earnings in a lifetime compare to those without an education.

Although a college education is crucial to living a better life, it has also been damaging not only those in debt, but also the economy. Attending school is beneficial, but students need to be more aware of their financial abilities when attending school.

Polonsky noted it is possible to deal with this debt when keeping on top of it.

data-animation-override>

“It is possible for people to live in this developed economy which allows people the basic level of survival to create debt. That’s the beauty of capitalist economy. The blame is on college here. College is very expensive and causes a very debatable proposition. The idea that a $60,000 private college is going to lead you to a better degree then a $30,000 public school is just a marketing technique used by the university.”

Student loan debt will always be an issue, and will worsen with the rise of interest rates. Students aren’t surprised about this debt until they are exposed to it after graduation.